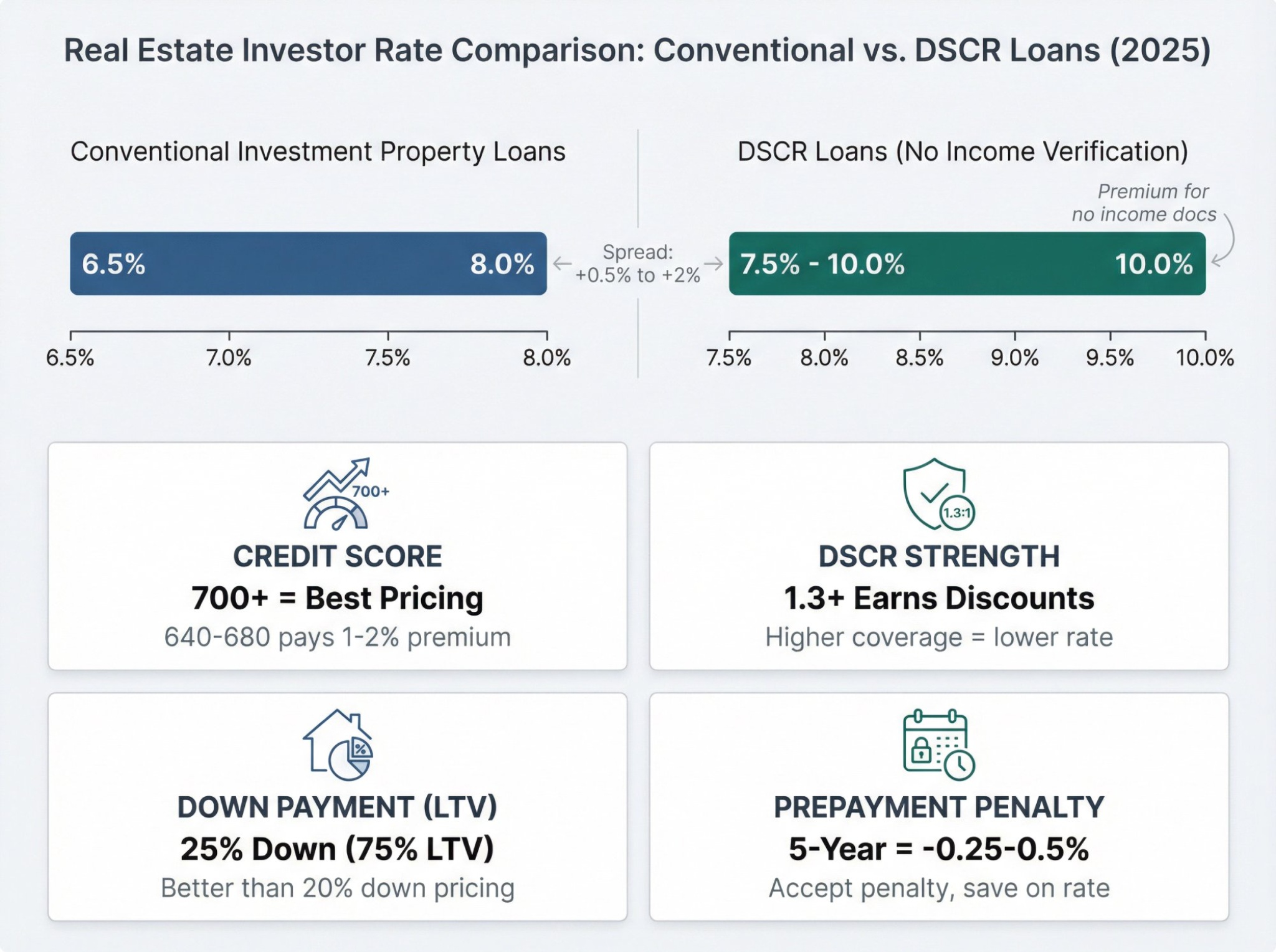

Debt Service Coverage Ratio (DSCR) loans continue to be a core financing option for real estate investors in 2026. While interest rates and rent assumptions often get the most attention, DSCR reserve requirements in 2026 have quietly become one of the most decisive factors in whether a DSCR loan gets approved—or denied.

Lenders are no longer relying solely on property cash flow. Liquidity and reserves now play a central role in underwriting, especially as markets normalize and operating risks remain elevated. If you’re evaluating long-term rental financing, start with an overview of our DSCR Loan Programs.

What Are Reserve Requirements in DSCR Lending?

Reserve requirements refer to the amount of liquid capital a borrower must hold after closing. These funds are typically expressed as a number of months of PITI (principal, interest, taxes, and insurance).

In earlier years, DSCR loans were attractive in part because reserves were minimal or waived entirely. That has changed.

DSCR reserve requirements in 2026 are viewed as a safety buffer rather than a formality.

Why Lenders Are Requiring More Reserves

Several factors are driving stricter reserve requirements:

1. Expense Volatility

Insurance premiums, property taxes, and maintenance costs have all become less predictable. Reserves give lenders confidence that short-term expense spikes will not immediately lead to payment stress.

2. Rent Softening in Select Markets

While many rental markets remain strong, lenders are underwriting defensively against potential rent plateaus or modest declines. Reserves help bridge temporary cash-flow gaps.

3. Portfolio Risk Management

Lenders are increasingly managing risk at the portfolio level. Requiring reserves across all loans helps reduce default risk during economic slowdowns.

4. Reduced Tolerance for Thin Margins

Deals that only barely meet DSCR thresholds are now expected to carry additional liquidity support.

Typical Reserve Requirements Investors Are Seeing in 2026

Although requirements vary by lender, common standards include:

- 6 months of PITI for single-property DSCR loans

- 9–12 months of PITI for short-term rentals or higher-risk markets

- Additional reserves for multi-property or portfolio loans

- Verification that reserves are liquid and accessible

In some cases, lenders also require reserves to be held per property, not pooled across a portfolio.

How Reserves Impact DSCR Loan Approvals

Reserve requirements can affect approvals in several ways:

- Loan denial despite strong DSCR: A deal may cash flow well but fail due to insufficient liquidity.

- Reduced leverage: Some lenders will lower LTV if reserve requirements are marginal.

- Delayed closings: Borrowers scrambling to source reserves often slow the approval process.

This is especially common for investors transitioning from renovation financing, such as Fix & Flip Loans, into long-term DSCR debt.

Common Investor Mistakes Around Reserves

Investors frequently run into issues by:

- Assuming reserves are negotiable or optional

- Counting illiquid assets (equity, retirement accounts without access)

- Moving funds before closing

- Failing to plan reserves at the portfolio level

These missteps are increasingly costly as lenders tighten consistency across loan files.

How Investors Can Prepare Without Killing Returns

Smart investors are adapting rather than resisting reserve requirements. Effective strategies include:

- Planning liquidity early during deal analysis

- Maintaining operating reserves outside of closing requirements

- Using conservative underwriting to reduce required reserves

- Staggering acquisitions to preserve liquidity

Many investors pair DSCR loans with a longer-term capital strategy, including Cash-Out Refinance Loans, once properties are stabilized.

Why Strong Reserves Can Actually Improve Deal Quality

While reserve requirements may feel restrictive, they often result in:

- More durable portfolios

- Lower default risk during market shifts

- Better lender relationships

- Greater flexibility during refinance or sale

From a long-term perspective, reserves improve both lender confidence and investor stability.

Final Thoughts: Liquidity Is Now a Core Underwriting Metric

In 2026, DSCR lending is no longer just about whether a property cash flows on paper. Liquidity matters.

Investors who plan for reserve requirements upfront are far more likely to secure approvals, close smoothly, and scale sustainably. As underwriting continues to evolve, disciplined capital management has become a competitive advantage—not a constraint.